You’ve booked your flight to India. The visa is approved. Your luggage is packed. But here’s what most travelers forget: a single medical emergency in India can cost more than your entire trip—sometimes much more. Without travel insurance, you could face bills of ₹3,00,000 to ₹50,00,000 (approximately $3,600-$60,000 USD) for evacuation alone. This guide shows you how to protect yourself with the right insurance, starting at less than $1 per day.

Is Travel Insurance Required for India?

Short answer: No, it’s not mandatory for US citizens visiting India on an e-visa or regular tourist visa. Unlike some European countries that require proof of travel insurance before entry, India doesn’t enforce this requirement.

But here’s the real question: Can you afford NOT to have it?

Without travel insurance, you’re personally liable for every medical emergency, lost flight, canceled hotel, and delayed baggage. Digestive issues? That’s your bill. A serious injury requiring hospitalization? That’s your bill. Missed flight connection? Out of pocket. The risk is simply too high when you’re traveling thousands of miles from home.

The Real Cost of Medical Emergencies in India (What Could Happen)

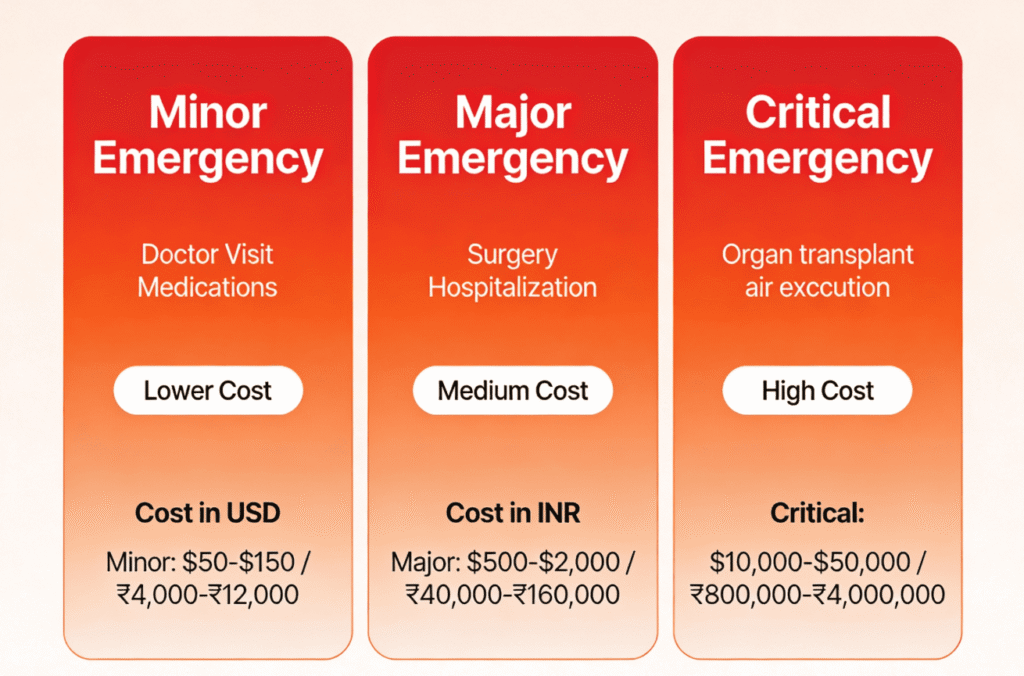

India has excellent hospitals, especially in major cities like Delhi, Mumbai, and Bangalore. But here’s the catch: you’ll pay out of pocket, and costs are rising fast. Here are real-world examples from 2025 medical data:

Minor Emergency: Doctor visit for food poisoning with IV fluids = ₹6,000-15,000 (approximately $72-180 USD)

Moderate Emergency: Broken arm surgery and hospital stay = ₹40,000-80,000 (approximately $480-960 USD)

Major Emergency: Heart attack with angioplasty (stent) = ₹3,00,000-8,00,000 (approximately $3,600-9,600 USD)

Critical Emergency: Organ transplant = ₹15,00,000-40,00,000 (approximately $18,000-48,000 USD)

Medical Evacuation: Air ambulance from remote area = ₹3,00,000-50,00,000 (approximately $3,600-60,000 USD)

The most frightening part? An air ambulance evacuation from a remote location (like Ladakh or a mountain trekking area) can cost ₹50,00,000 ($60,000 USD) or more—completely bankrupting you if not insured. Even evacuation from one city to another in India costs ₹3,00,000-8,00,000 ($3,600-9,600 USD).

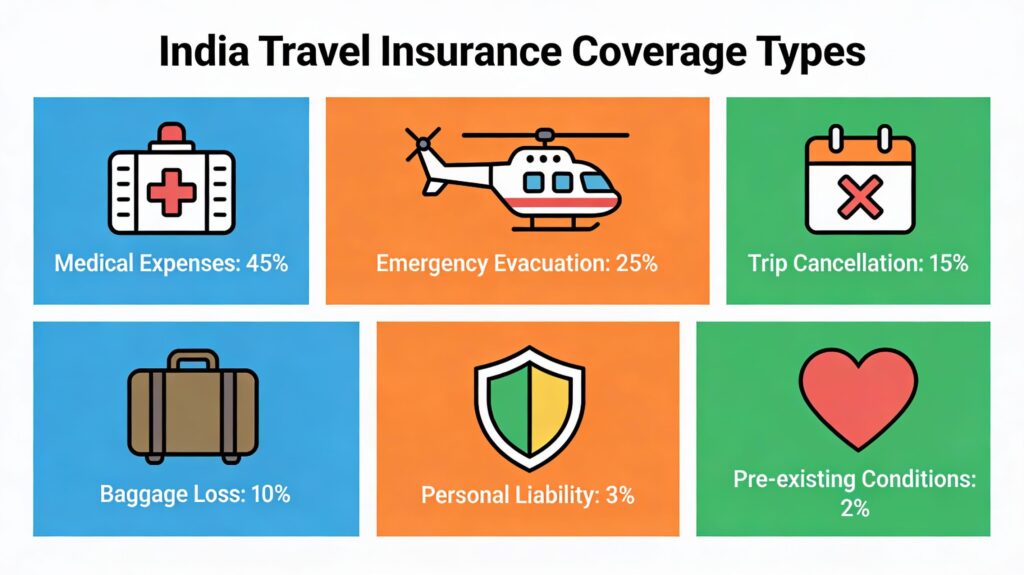

What Does Travel Insurance for India Cover?

Travel insurance isn’t one-size-fits-all. Different plans cover different things. Here’s what you need to understand:

Medical Expenses (Most Important)

If you fall ill or get injured while traveling in India, medical insurance covers your hospital bills, doctor visits, medications, and surgeries. Coverage ranges from ₹30,00,000 to ₹75,00,000 (approximately $36,000 to $90,000 USD) depending on the plan. Most travelers should target at least ₹50,00,000 ($60,000 USD) in medical coverage.

Emergency Medical Evacuation (Critical)

This is the big one. If you’re seriously ill or injured in a remote area (like trekking in the Himalayas or visiting rural villages), an air ambulance can transport you to a proper hospital—or all the way back to the US. Without insurance, this single evacuation can cost ₹3,00,000 to ₹50,00,000 ($3,600 to $60,000 USD). With insurance, it’s covered.

Trip Cancellation

If you have to cancel your trip for a covered reason (sudden illness, death in family, job loss, weather), trip cancellation coverage reimburses your prepaid, nonrefundable costs. This includes flights, hotels, tours, and activities. Coverage is typically 100% of your trip cost, up to a limit ($5,000 to $100,000 depending on plan).

Trip Delay & Interruption

If your flight is delayed 12+ hours or you have to cut your trip short, these coverages reimburse your accommodation and meal costs while stuck waiting for a new flight.

Baggage Loss & Delay

Airlines lose luggage. This coverage reimburses you for lost bags or covers immediate expenses (toiletries, clothing) if your baggage is delayed 12+ hours.

Passport Loss

Losing your passport abroad is a travel nightmare. Passport loss coverage reimburses the cost of emergency passport replacement and any emergency travel needed.

Personal Liability

If you accidentally damage hotel property or injure someone, personal liability coverage protects you from legal costs and damages (up to $100,000-$500,000).

How Much Does Travel Insurance for India Cost?

Good news: travel insurance for India is cheap. Here’s what you can expect to pay:

Budget Plans: ₹20-₹50 per day (~$0.25-$0.60 USD/day) or ₹300-750 for a 2-week trip

Mid-Range Plans: ₹60-₹125 per day (~$0.75-$1.50 USD/day) or ₹1,400-2,800 for a 2-week trip

Comprehensive Plans: ₹125-₹200 per day (~$1.50-$2.50 USD/day) or ₹2,800-4,200 for a 2-week trip

Average Traveler Cost: According to Squaremouth travel insurance data, the average US traveler spends about ₹1,000 per day, or roughly ₹22,000-24,000 for a 24-day trip to India (approximately $266-290 USD).

Put it in perspective: that’s less than a single nice meal at a restaurant in most Indian cities. For ₹22,000 ($266 USD), you get protection against medical bills of ₹50,00,000+ ($60,000+ USD) and evacuation costs of ₹50,00,000+ ($60,000+ USD). The math is simple: insurance is absolutely worth it.

Best Travel Insurance Plans for India: Our Top 5

1. Pathway Premium (Best All-Around Coverage)

Cost: $43-$126 for a 2-week trip (varies by age)

Medical Coverage: Up to ₹75,00,000 ($90,000 USD)

Trip Cancellation: 100% of trip cost (up to $100,000)

Medical Evacuation: Up to ₹75,00,000 ($90,000 USD) – Included

Best For: Travelers who want balanced coverage of both medical and trip cancellation

Why Choose It: Pathway Premium offers excellent trip cancellation coverage combined with solid medical protection. If you’re worried about losing your prepaid trip costs due to illness, this is your plan.

2. Atlas Essential (Best Budget Plan)

Cost: $27-$54 for a 2-week trip

Medical Coverage: ₹30,00,000 ($36,000 USD)

Trip Cancellation: Limited (not primary focus)

Medical Evacuation: ₹50,00,000+ ($60,000 USD) – Included

Best For: Budget-conscious travelers, young and healthy travelers, short trips

Why Choose It: This is the cheapest option while still covering emergency evacuation. If you’re young, healthy, and mainly want protection against catastrophic medical expenses, Atlas Essential is hard to beat.

3. iTravelInsured Travel LX (Most Flexible)

Cost: $50-$150 for a 2-week trip (varies by age and coverage)

Medical Coverage: Up to ₹3,75,00,000 ($450,000 USD)

Trip Cancellation: 100% (includes “cancel for any reason” option)

Medical Evacuation: Up to ₹3,75,00,000 ($450,000 USD) – Included

Best For: Older travelers, travelers with pre-existing conditions, luxury trip protection

Why Choose It: The “cancel for any reason” feature lets you get a refund if you simply change your mind—no need for a covered reason. High evacuation coverage is great for remote travel plans (mountain trekking, adventure tourism).

4. Patriot International Lite (Best for Expats/Long Stays)

Cost: $29-$214 for a 2-week trip

Medical Coverage: ₹30,00,000-1,50,00,000 ($36,000-180,000 USD) – depending on plan

Trip Cancellation: Varies by plan

Medical Evacuation: Included

Best For: Travelers on a budget, those staying 2-4 weeks

Why Choose It: Patriot International offers good coverage at low prices, especially for extended trips. Popular with backpackers and budget travelers.

5. Tata AIG (Best if Buying in India)

Cost: ₹24.80/day (~$0.30/day USD) or about ₹500-600 for a week

Medical Coverage: Up to ₹75,00,000 ($90,000 USD) – depending on plan

Trip Cancellation: Up to ₹75,000 ($900 USD)

Medical Evacuation: Included

Best For: Travelers buying insurance after arriving in India, budget travelers

Why Choose It: Cheapest daily rate available. Good if you’re already in India and realize you forgot insurance. Instant online purchase with no medical test required.

Key Features to Look for in India Travel Insurance

Medical Evacuation (Must Have)

This is non-negotiable if you plan to visit remote areas, trek in mountains, or travel during rainy season when roads become dangerous. An air ambulance evacuation without insurance can cost ₹3,00,000-50,00,000 ($3,600-60,000 USD). With insurance, it’s covered. Minimum recommendation: ₹50,00,000 ($60,000 USD) evacuation coverage.

Pre-Existing Condition Coverage (If Applicable)

If you have any chronic health conditions (diabetes, high blood pressure, asthma, etc.), make sure your plan covers pre-existing conditions. Some plans exclude them entirely, others cover them if declared upfront. Plans like Atlas America and Patriot America Plus specifically cover pre-existing conditions.

Cashless Medical Claims

Look for plans offering “cashless claims” or direct billing to hospitals. This means you don’t pay upfront and get reimbursed later—the insurance company pays the hospital directly. This is critical if you face a large medical bill.

24/7 Emergency Hotline

You want to reach someone immediately if an emergency happens—not during business hours. All reputable plans offer 24/7 helplines. This matters more than you think when you’re sick and need guidance on which hospital to go to.

Trip Cancellation Limits

If your trip costs $8,000, buy a plan that covers at least $8,000 in trip cancellation. Don’t buy a $5,000 limit plan for an $8,000 trip—you’ll only recover partial costs.

COVID-19 Coverage

Most plans now include COVID-19 coverage for medical expenses and trip cancellation if you test positive. Verify this is included before purchasing.

Common Situations That Travel Insurance Covers

You Get Food Poisoning

You ate something at a street vendor and got severe food poisoning. You need IV fluids and antibiotics at a local hospital. Cost: ₹6,000-15,000 ($72-180 USD). Travel insurance covers this under medical expenses.

You Get Dengue or Malaria

You were bitten by a mosquito and contracted dengue (very common in India). You need hospitalization and blood tests. Cost: ₹25,000-50,000 ($300-600 USD). Covered under medical expenses.

You Break Your Leg Trekking

You fell while trekking in the Himalayas. You need emergency evacuation to a major hospital, X-rays, surgery, and hospital stay. Cost: ₹1,50,000-4,00,000 ($1,800-4,800 USD). Medical evacuation insurance covers this entirely.

You Have to Cancel Your Trip

Your mother had a heart attack and you need to fly home. Your $3,000 flight and $2,000 hotel are non-refundable. Trip cancellation insurance reimburses you $5,000.

You Miss Your Flight Connection

Your international flight from US is delayed 15 hours, causing you to miss your connecting flight to India. You need a new hotel for the night and a new connecting flight. Cost: $500-$1,500. Trip delay insurance reimburses this.

Your Luggage Gets Lost

The airline loses your checked bag for 48 hours in Delhi. You need to buy emergency toiletries, clothing, and medications. Cost: ₹5,000-8,000 ($60-96 USD). Baggage delay coverage reimburses this.

What Travel Insurance Does NOT Cover (Important)

Travel insurance is powerful, but it’s not a blank check. Here’s what typically is NOT covered:

Pre-existing conditions (unless declared): If you have high blood pressure and it wasn’t declared when buying insurance, a stroke caused by that condition won’t be covered.

Travel against medical advice: If a doctor told you not to travel, you can’t then buy insurance and claim a related illness.

High-risk activities (unless added): Mountaineering, extreme sports, professional athletics. You need “adventure sports” add-ons for these.

Claims due to alcohol or drug use: If you were drinking and got injured, coverage may be denied.

Travel to countries under government warnings: If the US State Department advises against travel to a location, insurance won’t cover claims there.

Claims caused by failure to get required visas: If you didn’t get a visa and had to cancel, that’s not covered.

Non-emergency medical tourism: Elective cosmetic surgery or planned procedures are not covered (only emergencies).

How to Choose the Right Plan

Step 1: Define Your Trip Cost

Add up flights, hotels, tours, meals, and activities. Let’s say your total trip cost is $4,000. You want trip cancellation coverage of at least $4,000.

Step 2: Assess Your Health Status

Are you young and healthy? Budget plan is fine. Have pre-existing conditions? Look for Atlas America or Patriot America Plus. Over 65? Consider iTravelInsured LX for higher limits.

Step 3: Consider Where You’re Going

Major city (Delhi, Mumbai, Bangalore)? Standard plans work. Remote area (Ladakh, Northeast states, small villages, mountain trekking)? Get higher medical evacuation coverage (₹50,00,000+).

Step 4: Check Coverage Limits

Medical coverage should be at least ₹50,00,000 ($60,000 USD). Medical evacuation should be at least ₹50,00,000-1,50,00,000 ($60,000-180,000 USD). Trip cancellation should match your trip cost.

Step 5: Buy with Deductibles in Mind

Lower deductibles ($0-$100) are better but cost more. Higher deductibles ($250+) cost less but you’ll pay that amount out of pocket for each claim.

When to Buy Travel Insurance for India

Best Time: Within 14 days of booking your first trip payment (flight, hotel, or tour). This ensures you get the best rates and maximum coverage options.

Last-Minute Buying: You can buy travel insurance right up to your departure date, but some plans aren’t available if you wait too long. Don’t wait.

Multi-Trip Plans: If you travel to India multiple times per year, annual multi-trip policies are cheaper than buying separate policies each time.

Top Travel Insurance Providers for India

For US citizens traveling to India, these providers consistently rank highest in reliability, claims processing, and customer service:

- IMG (iTravelInsured): Excellent customer service, flexible plans, include “cancel for any reason” options

- World Nomads: Popular with backpackers, instant purchase, covers adventure activities

- Pathway Insurance: Simple plans, great trip cancellation coverage, easy claims process

- Atlas Travel Insurance: Cheapest options, good medical evacuation, popular with budget travelers

- Patriot Insurance: Good pre-existing condition coverage, reliable claims processing

- Tata AIG: If buying in India, cheapest daily rate, instant coverage

Pro Tips Before Your Trip

Read the Policy Carefully: Don’t assume coverage—read your actual policy document. Exclusions are in the fine print.

Keep All Receipts: Save all medical receipts, hotel confirmations, and flight documents. You’ll need these for claims.

Make a Copy of Your Insurance Card: Screenshot your insurance policy details and email them to yourself. Keep a physical copy in your wallet.

Know Your Hotline Number: Write down your insurance company’s 24/7 emergency hotline. Save it in your phone with “INSURANCE” label.

Declare Pre-Existing Conditions: If you have any health issues, declare them during purchase. Undisclosed conditions won’t be covered.

Buy from Official Websites: Don’t buy travel insurance from random sites. Use the official insurance company website or trusted comparison sites like Squaremouth or InsureMyTrip.

Your Next Step: Protect Your Trip

Travel insurance for India isn’t an expense—it’s an investment in peace of mind. For less than ₹100 per day (about $1.20 USD/day), you protect yourself against medical bills of ₹50,00,000+ ($60,000+ USD) and evacuation costs of ₹50,00,000+ ($60,000+ USD).

Here’s what to do right now:

- Calculate your total trip cost (flights, hotels, tours, meals)

- Choose a plan that matches your budget and risk tolerance

- Buy it today (don’t wait)

- Save your policy details and emergency hotline

- Travel with confidence knowing you’re protected

You’ve worked hard to plan this trip to India. Don’t let a single medical emergency or flight cancellation ruin it. Get insured, travel smart, and enjoy the experience.

Ready to book your trip? Read our complete guide on how to get your Indian e-visa online and plan your India travel budget. Also consider booking hotels in advance to save money on accommodation.